Executive Summary

The Russian-Chinese economic relations experienced a sharp dip in the immediate months after Russia’s full-scale invasion of Ukraine in February 2022, but has since rebounded and reached new record levels, and grown strongly and widely in both directions, and in many areas:

- Bilateral trade turnover reached a record high of USD 190 billion in 2022 (29 percent up on 2021), and USD 94 billion in the first five months of 2023 (41 percent up on 2022).

- Russian energy export to China has increased moderately in volume, in line with pre-war plans, but massively in value, including oil, pipeline gas and LNG, and coal. However, no progress has been made on new infrastructure, and no new Chinese investments upstream. As China profited less than it could have, the largest energy winner has instead been India.

- The countries’ metals trade has grown much. Russia is selling gold, platinoids, copper, and steel, while China is exporting alumina – which has crucial military applications.

After an initial post-invasion decline, Chinese exports to Russia have significantly increased since the summer of 2022, including vehicles, machinery, electronics, metals, and plastics and rubber.

- Most major Chinese companies have continued their operations in Russia as before. This includes banks, technology companies, industry and construction companies, and others. While sanctions have had an effect on some companies, actions do not always follow words.

- There has been a huge comeback over the past year in Chinese electronics exports such as smartphones, laptops, televisions, and refrigerators to Russia. Crucially, Chinese official and unofficial exports of the militarily important integrated circuits have skyrocketed. China has thus revived Russian electronics markets, and partly met some Russian technology needs.

- The strongest Chinese export category of 2023, driving export growth, is motor vehicles, including cars, trucks, and parts, where Chinese brands have entirely swallowed up the Russian markets, allowing China to become the world’s leading car exporter.

At the same time, the war has also shown the limits and challenges of the countries’ economic relations, as well as Russia’s increasing economic dependence on China, which in the long run could likely be the biggest threat to Russian sovereignty:

- Russia is undergoing increasing “yuanisation,” where the yuan’s role in Russia’s economy is growing, which might mitigate sanctions but entails risks and vulnerabilities vis-á-vis China.

- Russia’s isolation and dependence on China means a bleak future for the Russian state and its people: the exports to China are discounted, the imports are of lower quality and more expensive, and investments are absent. Growth, state budget and spending will all suffer.

- While China has exported many products with crucial military applications, it has not delivered lethal weapons, which is a clear limitation in Beijing’s support to Moscow.

The trends of growth in trade and economic relations, and of Russia’s dependence on China will likely continue. How strong the economic relations can grow will depend on many things: the outcome of the war; the power dynamic and balance between Moscow and Beijing; the ability of the West to counteract and punish China’s sanctions-busting; how China’s relations with the West develop overall; and how well China manages to balance and diversify its economic ties.

Introduction

In a joint statement on February 4, 2022, the leaders of China and Russia, Xi Jinping and Vladimir Putin, respectively, described the relationship between their countries as a friendship “without borders” and “without forbidden areas of cooperation.” Just three weeks later, on February 24, Russia initiated its full-scale invasion of Ukraine, thereby triggering the bloodiest conflict in Europe since World War II. This has put the alleged boundlessness of the relationship to the test. China has had to respond to the world’s condemnation of Russian actions, American and European demands to refrain from supporting Russia, and sanctions aimed at the Russian economy, which have also affected China.

Russia's invasion of Ukraine has also spotlighted a Russian-Chinese alliance whose ultimate goal extends far beyond Ukraine, namely, to replace the US-led liberal world order with a new “multipolar world order” that is safer for authoritarian states. When Xi visited Moscow in March 2023, he told Putin that “this is part of the great changes not seen in a hundred years” – a phrase often uttered by Xi Jinping and other Chinese representatives in recent years, but this time with the addition that Russia and China are “together promoting these changes”.

In order to assess the countries’ abilities to realise their joint ambitions, it is of utmost importance to identify and evaluate both the strengths and weaknesses of their cooperation. A deep understanding of the limitations in the relationship is a prerequisite for the EU and the West to develop a sustainable, objective, and long-term policy towards Russia and China.

Analyses of Russo-Chinese relations since the beginning of the war have often emphasised how China has provided extensive political support to Russia, primarily in the form of rhetoric. And even though it is often pointed out how China has provided an “economic lifeline” to Russia, there is a need for a more detailed analysis of how their bilateral economic relations have developed in various areas of cooperation. Overall, the answers to these questions can contribute to a better understanding of both areas of conflict and driving forces in Russo-Chinese relations.

This report, the first in a series on this topic, aims to analyse how Russo-Chinese economic relations have developed since the start of Russia’s war against Ukraine. The report thus covers bilateral trade, including Russia’s vital energy export to China, and China’s export to and economic presence in Russia; Russia’s increasing use of the yuan; cooperation on trade routes; and trade across the border and between regions.

Trade Data

Strong increase in bilateral trade during 2022 and 2023, in both directions. According to Chinese customs data[1] for 2022, the total trade between the countries reached a record high of about USD 190 billion, which is an increase of 29.3 percent compared to 2021; however, Russian exports (about USD 114 billion) accounted for a large majority of the increase (43.4 percent), while Chinese exports (about USD 76 billion) increased by 12.8 percent. Trade with Russia accounted for 3 percent of China’s total international trade in 2022. The strong upward trend has continued in 2023: in the first five months, bilateral trade turnover was about USD 94 billion, 40.7 percent higher than in the same period in 2022. In March 2023, trade reached its highest level ever; for the first time, it was over USD 20 billion in a month.

Moreover, unlike during 2022, in 2023 the increase in trade has been driven more by strong growth in China’s exports than Russia’s – up 67 percent, compared to 25 percent for Russia. In April 2023, China’s exports to Russia reached an all-time high of USD 9.6 billion, for the first time higher than Russian exports to China.

Figure 1: China’s trade with Russia turnover; exports; and imports. Source: Chinese customs.

Energy Trade – Russian Export to China

The export of energy from Russia to China has increased significantly in both volume and value since the outbreak of the war. Despite Russia’s being forced to export heavily discounted energy to China, due to sanctions, embargoes, and price ceilings, the value of energy exports has increased very strongly. Since the start of the war, China has imported Russian fossil fuels for about EUR 86 billion[2] (of which an overwhelming majority, about EUR 67 billion, is oil imports). In 2022, the value of Chinese imports of Russian oil, coal, LNG and pipeline gas was 56 percent higher than in 2021. China is thus the largest importer of Russian energy, after the EU bloc, since the start of the war, and the largest single country. However, the imbalance in energy relations has increased sharply; as outlined in the NKK/SCEEUS report Russia-China energy relations since 24 February: Consequences and options for Europe by Henrik Wachtmeister, the value of China’s share of Russian energy exports has doubled, from 15 to 30 percent, while Russia’s share of Chinese imports has only increased slightly.

China is now Russia’s biggest consumer, and Russia’s energy exports to China are likely to continue to increase in the future. At the same time, this Russian dependency on a single main customer poses great risks to the balance of power. Moreover, Chinese imports will probably not be able to replace Russian losses in European oil and gas markets.

Russian oil export to China: Since the outbreak of the war, China has imported Russian oil for about EUR 67 billion. Since April 2022, China’s discount on Russian oil has averaged 11 percent. Chinese import of Russian crude oil has increased during the war, and was 8.3 percent higher in volume in 2022 than in 2021, and 44 percent higher in value. In 2022, Russia was China’s second-largest supplier of crude oil, after Saudi Arabia, with 1.73 million barrels per day (mb/d), which accounted for a much larger share of Russian exports than of Chinese imports (see Table 1).

The upward trend has continued in 2023, as Chinese import of Russian crude oil averaged 1.95 mb/d in the first four months of 2023 (18 percent of Chinese imports). As of June, China is the top importer of Russian oil in 2023, at more than EUR 21 billion worth of imports and, in March 2023, imports reached record volume levels, at 2.27 million barrels per day, 1.5 times higher than in March 2022, but only 3 percent higher in value, reflecting the likely discounted price. Russian oil from the Arctic is also increasingly exported to China, with record volumes in March 2023. Chinese import of Russian Heavy Fuel Oil (HFO), which independent Chinese refineries import to produce diesel and gasoline, more than doubled in 2022 (3.1 million tons), and saw record volumes in February 2023.

Interestingly, China seems to have acted in an inexplicable way in its oil strategy during 2022, by strongly supporting Russia economically and politically, despite high costs for both its own and the world’s economies. It has done so by filling its reserves with imported Russian oil when it was at its most expensive, and then refraining from further exporting refined products, despite high margins and good conditions, which further contributed to global inflation and thus helped Russia.

Russian gas export to China: During the war, China has imported Russian gas for about EUR 12 billion. In terms of volume, China’s import of Russian pipeline gas rose by 50 percent in 2022 (totalling 15.5 billion cubic meters (bcm)), and Russian LNG, by 44 percent (totaling 6.5 million tons). In terms of value, the import of Russian pipeline gas increased by 160 percent in 2022, to about USD 3.98 billion, and the import of Russian LNG by 140 percent, to USD 6.75 billion.

Russia was thereby China’s second-largest supplier of pipeline gas in 2022, and fourth-largest supplier of LNG in 2022. The Russian export of pipeline gas to China is a much larger share of Chinese imports than Russian exports, as shown in Table 1, but the share in Russian exports increased significantly in 2022. Russia also more than doubled its export of Liquefied Petroleum Gas (LPG) to China in 2022, compared to 2021 (147,000 tons compared to about 63,000 tons). While Russian pipeline gas is China’s cheapest source of gas, Chinese imports have in general still only been increasing in line with plans that have existed since before the war.

Russian export of coal, electricity, and nuclear power: China has imported discounted Russian coal for a total of about EUR 7.2 billion since the beginning of the war. Imports rose by 20 percent in volume in 2022, and have also been increasing in 2023. Russia was China’s second-largest supplier of coal in 2022 and accounted for 23 percent of Chinese imports (up from 18 percent in 2021) and 32 percent of Russia’s exports (up from 25 percent in 2021), thus rising significantly in both countries’ trade mixes. Chinese imports of electricity from Russia also increased in 2022, compared to previous years. China is also an increasingly important market for the Russian state-owned nuclear power company, Rosatom, although the power balance in the nuclear power cooperation is increasingly shifting in China’s favour.

Energy trade infrastructure: An increase in Russian oil imports to China is limited, given that China is already buying essentially everything that Russia can deliver to the Pacific market, and requires either long and costly transports from Russia’s western ports, or new infrastructure. Similarly, the gas export is also limited by the fact that the Russian gas fields supplying Europe are not yet connected to those that supply China.

Several infrastructure projects are planned, or ongoing, to increase Russian energy export capacity to China. On 4 February 2022, the countries signed a new 30-year agreement on the export of Russian gas via a new pipeline from Sakhalin to China through the Sea of Japan, with a maximum capacity of 10 bcm, which would be operational within a few years. In January 2023, a new agreement was signed, with additional details. In September 2022, Russian Energy Minister Alexander Novak announced that the countries would soon reach a final agreement on the long-planned Power of Siberia 2 gas pipeline, which, from 2030, would be able to deliver an additional 50 bcm of Russian gas annually to China via Mongolia.

However, 2022 and 2023 have seen little progress in these and other projects, apart from empty Russian announcements and Chinese silence. In March 2022, it was reported that Chinese Sinopec paused several major energy projects in Russia, after China’s Ministry of Foreign Affairs, according to sources in a meeting with the three Chinese energy giants, Sinopec, CNPC, and CNOOC, urged caution with investments in Russia. “Arctic LNG 2,” a joint project between Russian Novatek and Chinese companies, has been delayed due to sanctions. At the end of 2022, it was reported that the Power of Siberia pipeline would reach full capacity two years later than planned.

Moreover, during the war, Chinese companies have not made any new upstream investments, nor have there been any announcements of new deals in oil, or gas, or long-term import contracts.

Chinese Exports to and Economic Presence in Russia

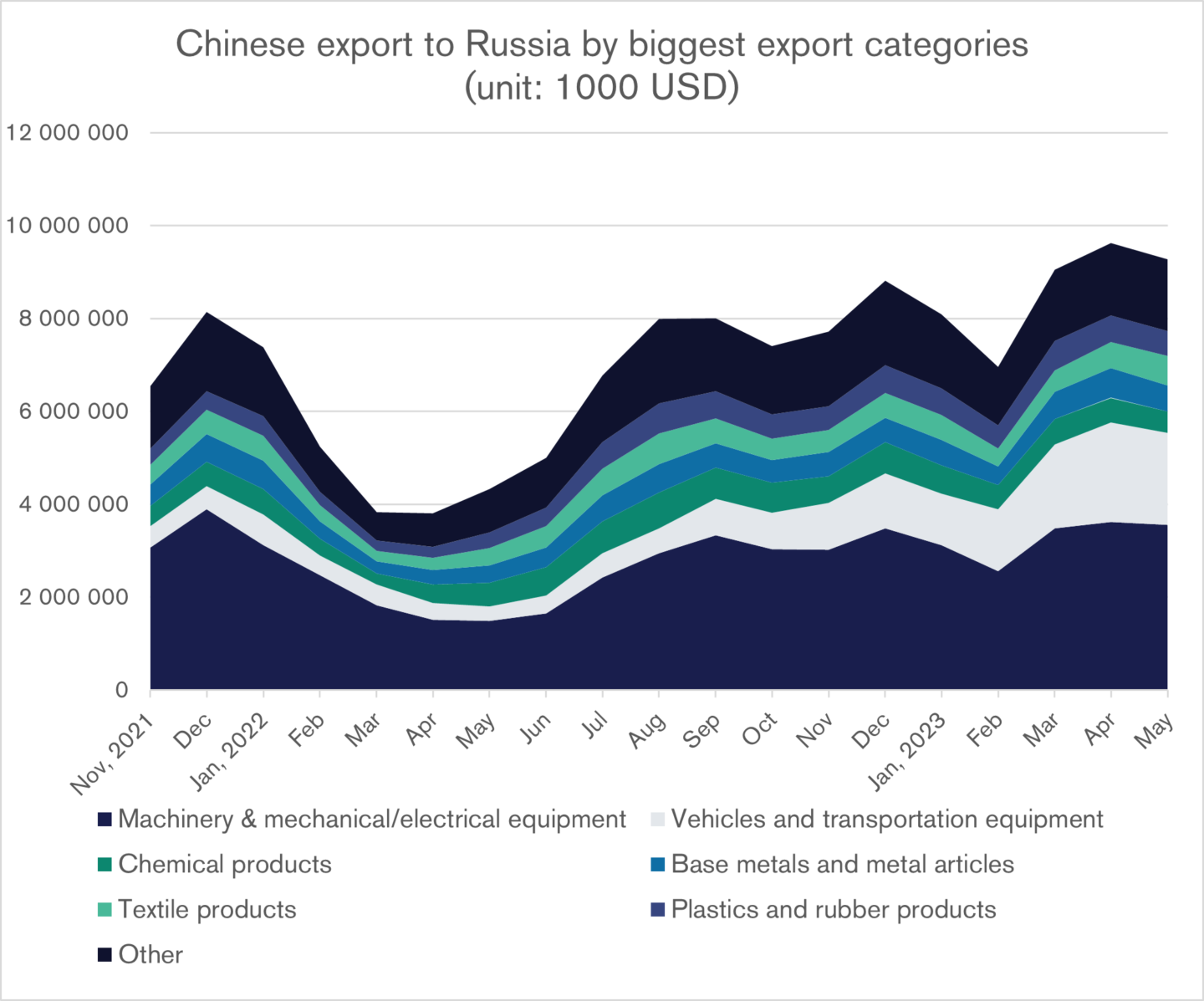

After some decline immediately following the start of the war, Chinese exports to Russia have heavily increased since the summer of 2022. Many Chinese products and brands have seen significant growth in Russia since the invasion, as can be seen in Figure 2. This includes significant export growth in categories such as vehicles; machinery and mechanical equipment; electronics, including consumer electronics, home appliances, and integrated circuits; metals; plastics and rubber; and many other goods and services.

Figure 2: Chinese export to Russia by biggest export categories (Harmonised Standard, HS, sections). Source: Chinese customs.

Chinese exports to Russia decreased sharply in the months following the war (from March to May, exports were 42 percent lower, compared to the previous three months) and were in line with the average for other countries that did not join the sanctions. But from July onwards, exports have increased sharply, and broadly, and reached their highest level ever in April 2023 (about USD 9.6 billion), for the first time higher than Russian exports to China. China has thus become Russia’s top trading partner, and only North Korea is now more dependent on Chinese exports.

The biggest product categories of China’s exports to Russia in 2022/2023 (categorised by their Harmonized Standard (HS) code), are the following: machinery and mechanical and electrical equipment; vehicles and transportation equipment; chemical products; base metals; textile products; and plastics and rubber. As can be seen in Table 2, the categories that saw biggest growth in 2022 were vehicles, chemicals, and plastics and rubber.

In the first five months of 2023, Chinese exports reached almost USD 43 billion. This was 75.6 percent higher than the same period in 2022, and 8 percent higher than the previous five months. This reflects the severe dip in exports in the months after the war, and that the sharp rebound in the second half of 2022 has slowed down to a more moderate growth in 2023. This can be clearly seen in Table 2, where all export categories show very strong growth figures in 2023, compared to the same period in 2022 (Jan–May), but low (or even negative) growth compared to the preceding five months (Aug–Dec). The clear exception is the export of vehicles and transportation equipment, which has continued to skyrocket in 2023 and is now the main driver of growth in China’s exports to Russia.

Most major Chinese companies are continuing their operations in Russia as before. According to Yale’s CELI list, and KSE Institute’s “Leave Russia” Project, which track foreign companies’ operations in Russia, almost all major Chinese companies are continuing their activities as before. This includes Air China; Alibaba; Tencent; China Mobile; China Railway; major banks (Agricultural Bank of China, China Construction Bank, Industrial Bank China); technology companies (Xiaomi, Haier, Realme, Oppo); energy companies (PowerChina, CNPC, PetroChina, Hengli Group, CCTD); construction companies (China Railway Construction Corporation, China State Construction Engineering); industrial companies (Didi, FAW, SAIC Motor, Xibao); and many others. Since the start of the war, several Chinese companies, including the metallurgy giant, Xibao, the leading producer of household appliances, Haier, the electric car company, Sokon, and the construction giant, CCCC Dredging, have begun planning their own manufacturing in Russia. Interestingly, Chinese companies have even faced domestic backlash against plans to limit Russian operations.

However, sanctions have had an (uncertain) effect on the operations of a few major Chinese companies. The Chinese companies that have curtailed operations in Russia are mainly high-profile, with important Western relations and global sales, and thus facing pressure to comply with sanctions. Companies that have (at least partially) limited their operations, or are buying time, include Huawei, ZTE, Honor, Lenovo, UnionPay, Bank of China, Asian Infrastructure Investment Bank, Industrial and Commercial Bank of China (ICBC), New Development Bank, Sinopec, and AliExpress (including the blocking of Russian drone purchases).

At the same time, actions do not always follow words. UnionPay significantly increased its operations with Russian customers outside Russia, and Russian banks, in 2022 (but seems to have limited operations again, as of May 2023). Both the Bank of China and the ICBC, through daughter companies, sharply increased both their activities, and profit, in Russia in 2022. Binance, which first limited its services for Russians, removed these limits in April 2023. In April 2022, Chinese drone company SZ DJI reportedly paused its operations in Russia, due to sanctions, but trade data has since showed that the drones have continued to flow into Russia through third countries. While Huawei has taken several steps to limit its Russia operations, other actions suggest it plans to remain, somehow, on the Russian market, including through increased efforts to recruit Russian talent, and engaging in joint Russian-Chinese IT development.

With growing sanctions pressure on Russia, and worsening Western-Chinese relations, avoiding sanctions might become increasingly difficult for Chinese global and state-owned companies. However, Chinese companies, especially smaller, second-rate, and regional companies are also learning to adjust. As with the earlier sanctions since 2014, Chinese businesses seem to be taking advantage of the short-term gains of the Russian market, while striving to comply with sanctions.

Electronics. The war and the sanctions had a strong initial effect on Chinese electronics exports to Russia in the spring of 2022; these exports included consumer electronics, such as laptops, smartphones, and TVs; telecommunications equipment; household appliances, such as washing machines, refrigerators, and ovens; and also the militarily important, dual-use category of integrated circuits (microchips) and semiconductors. However, since the summer of 2022, all of these categories have bounced back, many of them to new record levels, as is shown in Figure 3, with UN Comtrade data of 2021–2022. As with China’s exports to Russia, in general, this trend has continued in 2023, as the export of machinery and electronics has remained at high levels, as can be seen from the Chinese customs data in Figure 2.

Figure 3: Chinese exports to Russia of some major electric appliances (HS subcategories in chapters 84–85). Source: UN Comtrade.

The export of household appliances has greatly increased in the second half of 2022, filling the void left by the greatly reduced export from the Western world. As can be seen in Figure 3, the export of refrigerators and freezers, electric ovens and stoves, vacuum cleaners, and electric fans, have all increased during the second half of 2022 and reached pre-war levels in terms of value.

Figure 4: Chinese exports of laptops (HS 847130) to Russia 2021–2022. Source: UN Comtrade.

The same trend is true of consumer electronics. As can be seen in Figure 4, the Chinese exports of laptops dipped to almost zero in the months after the invasion, but have since experienced a significant comeback. Chinese export of televisions reached a low point in April 2022, but has since skyrocketed to record highs. In Russia, the sales of Chinese smartphones, which, with such giants as Xiaomi, Realme, Honor, Huawei, and Oppo, account for a majority of the Russian market, declined sharply in the spring, due to sanctions and the collapse of the ruble. However, since the summer of 2022, many Chinese tech companies have greatly increased their smartphone sales in Russia, up to and beyond pre-war levels, and largely filled the gap left by Western (and some Chinese) companies. This has led to a recovery in the Russian market, even though the value of imports is lower, due to cheaper Chinese brands. Chinese smartphones made up more than 70 percent of the Russian market in the third quarter of 2022 and, according to some sources, more than 95 percent, as of the first months of 2023, compared to around 40–50 percent before the war, with Xiaomi and Realme in the first two spots.

Figure 5: Chinese exports to Russia of integrated circuits (HS 8542) and semiconductors (HS 8541) 2021–2022. Source: UN Comtrade.

In particular, the critical export of Chinese integrated circuits and semiconductors to Russia has greatly increased. These dual-use products are extremely important for military uses and Russian defense industrial capacity. Russian semiconductor imports declined significantly shortly after the invasion and the sanctions, as 90 percent of the global exports to Russia of these categories disappeared. However, after an initial sharp decline, Chinese exports to Russia of integrated circuits have skyrocketed since April 2022, as can be seen from UN Comtrade data in Figure 5, thus partially filling the gap. In Chinese customs data, the value of integrated circuits exports to Russia in 2022 was USD 179 million, 142 percent higher than 2021 (USD 74 million).

However, many reports suggest that the true value of these exports from China to Russia could be much higher, owing to shadowy alternative Chinese routes to Russia, through third countries, and other shady trade setups. According to a report by the Free Russia Foundation, China’s and Hong Kong’s real exports of integrated circuits and semiconductors to Russia in 2022 were over USD 500 million and USD 400 million, up around 150 and 100 percent respectively, from around USD 200 million each in 2021. In China’s export of integrated circuits to Russia, both Hong Kong and third countries, such as Turkey, play important roles. Some sources suggest that China and Hong Kong accounted for almost 85 percent of Russian chip imports between March 2022 and February 2023.

Moreover, according to Nikkei Asia, the export from Hong Kong and China to Russia of U.S. chips, such as those by Intel and Texas Instruments, jumped tenfold from 2021 to 2022, reaching USD 570 million. Leaked Russian customs data reveal that, by late 2022, Russia’s microchips imports were close to pre-war levels, of which more than half were Chinese. However, China has also banned the export of certain semiconductors that have important military and strategic significance.

Although those Chinese microchip manufacturers that are most dependent on Western equipment (e.g., SMIC) have been cautious about circumventing the sanctions, Chinese companies that instead repackage products have increased their operations. However, the Chinese products do not have the same capacity as the Western ones and are not sufficient to fully cover Russia’s needs. According to some reports, the number of defective microchips and components imported from China to Russia has also increased, from two to 40 percent.

Thus, China has successfully, but also selectively, so as not to be affected by sanctions, managed to meet several of Russia’s large electronics and technology needs. China’s increasing exports, since the summer of 2022, might be partly due to increased Chinese confidence in managing and circumventing the sanctions, as both the red lines, and limits, of the sanctions regime have been drawn more clearly.

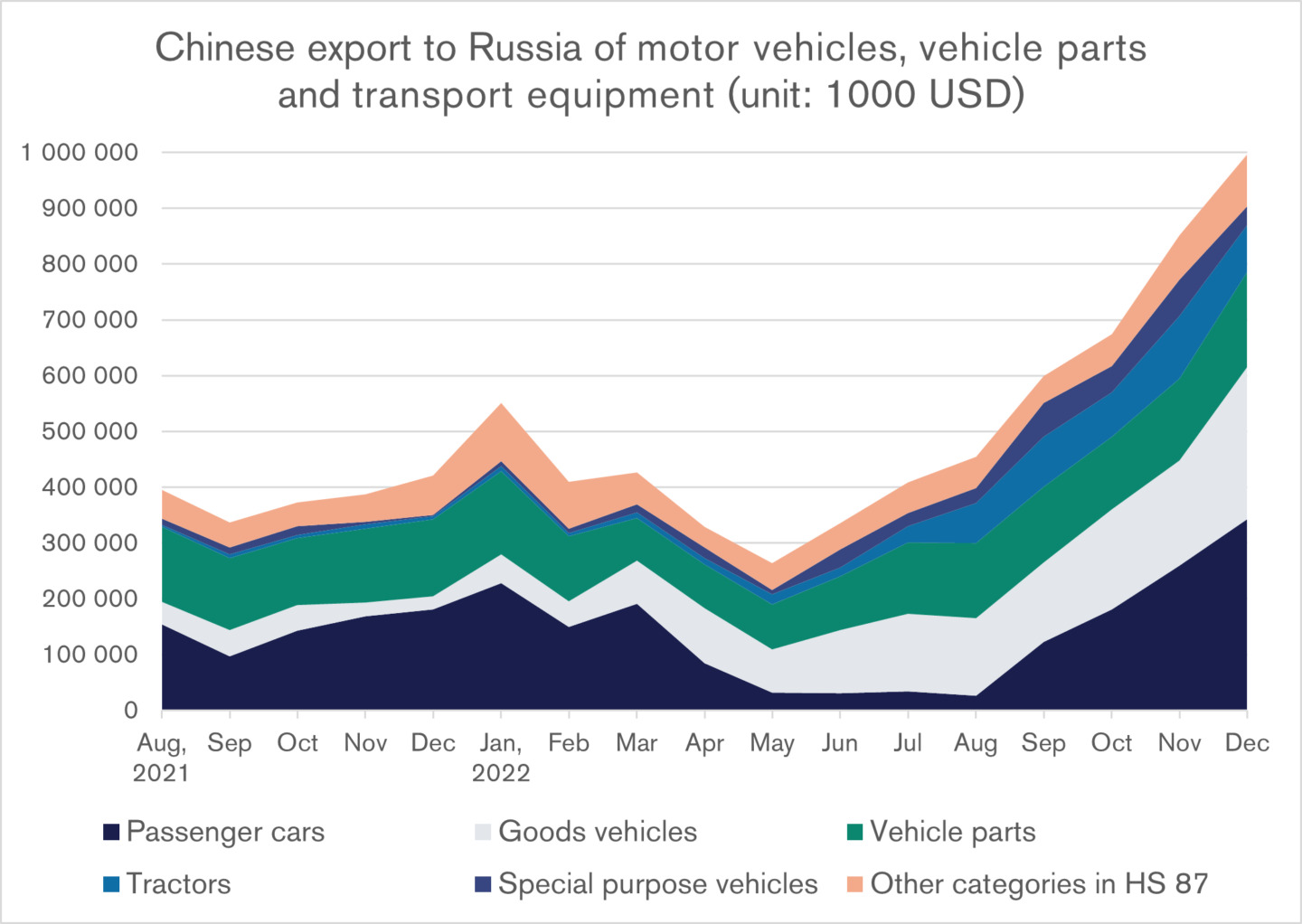

Vehicles. China is selling an increasing number of motor vehicles, vehicle parts and transportation equipment to Russia. According to Chinese customs data, the export to Russia of road vehicles, including parts and accessories, in 2022 (USD 6.3 billion) increased by 47 percent compared to 2021. As shown in Figure 6, this strong upwards trend has continued in 2023. This export category, China’s second-largest to Russia, accounted for 18.5 percent (USD 8 billion) of total exports in Jan–May 2023, 300 percent higher than in the same period in 2022, and 122 percent greater than in the preceding five months. Much owing to this export to Russia, now China’s top export trade partner in this category, in the first quarter of 2023, China became the world’s biggest exporter of new vehicles, overtaking Japan.

Figure 6: Chinese exports to Russia of road vehicles (HS chapter 87), 2022–2023. Source: Chinese customs.

China’s export to Russia of vehicles and transport equipment in large part consists of a few big subcategories: tractors, motor vehicles for the transport of persons (passenger cars), motor vehicles for the transport of goods (goods vehicles/trucks), special purpose motor vehicles, and parts and accessories for motor vehicles (vehicle parts). As clearly seen in Figure 7, all these categories have rebounded since the low of May 2022, and especially the export of passenger cars, trucks, and tractors has exploded since then, and are now main drivers in the increasing overall Chinese exports to Russia.

Figure 7: Chinese exports to Russia of road vehicles (HS chapter 87) by biggest subcategories, 2021–2022. Source: UN Comtrade.

The large Russian passenger car market was also hit hard by the war and sanctions and, during the first few months, Chinese exports to Russia of cars (such as Chery, Changan, Naval, and Geely[3]) declined sharply. However, the trend reversed and in November 2022, Chinese companies exported 20,000 vehicles to Russia, an amount 70 percent higher than in November 2021, and had a market share of 31 percent, compared to 10 percent a year before. This figure could reach 40 percent in 2023. Out of an original 60 brands, only 14, of which 11 were Chinese, remained in Russia at the end of 2022. In March 2023, Chinese car companies established an industry association to facilitate entry into the Russian market. Several Chinese companies, including Kaiyi, Hongqi and Tank, have plans to expand on the Russian market,. Reportedly, Chinese car models are also being rebranded and sold as Russian.

The sale of Chinese trucks (of which 90 percent are accounted for by four brands: Shaanxi, Howo, JAC, and FAW) more than quadrupled in 2022, compared to 2021 (31,000 versus 7,700 vehicles), after the Russian market largely collapsed, due to the withdrawal of European companies after the invasion. The share of Chinese trucks on the Russian market reached over 50 percent in January 2023, thus replacing even Russian brands. In addition, China has taken over as the main exporter of vehicle parts to Russia, from 17 percent of Russia’s imports, in 2021, to 59 percent in 2022.

Trade in metals. The two countries’ bilateral trade in metals has increased greatly since the invasion. China’s export of base metals, which dipped following the invasion, grew back strongly, and was 41 percent higher in 2023, as seen in Table 2. Importantly, Chinese export of alumina, crucial for military products, has increased thousand-fold since 2022, since the cessation of exports from Ukraine and Australia to Russia. Alumina (aluminium oxide) is used to produce aluminium, which in turn is crucial for defense industrial production. In all of 2021, China only exported 1,747 tons of alumina to Russia, but, in 2022, a total of 843,000 tons were exported, and China thus became a net exporter, for the first time in a long while.

Figure 8: Chinese export to Russia of alumina (HS 281820) 2021–2022. Source: UN Comtrade.

This also enabled the Russian aluminium giant, Rusal, to continue its production, despite problems with supply chains. This, in turn, enabled Russia to increase its export of aluminium to China significantly, by 56 percent, in 2022, compared to 2021, and rise from 18 to 69 percent of Chinese imports. In April 2023, Chinese imports of Russian aluminium nearly tripled, compared to April 2022. In 2022, Chinese imports of Russian alloy also rapidly rose, by 71 percent, to 57 000 tons; during 2022 and 2023, a Chinese company even bought copper alloys from Russian-occupied parts of Ukraine.

Russian export of metals to China has increased sharply during the war. China’s import of Russian gold increased in volume by about 67 percent in 2022, to a value of USD 387 million. During the war, Chinese imports from Russia, of both platinum metals and refined copper, have also increased, and in 2022, Russia’s export of semi-finished steel increased in volume by 300 percent, equivalent to USD 1.34 billion.

Other goods: ATMs, airplane parts, legal services, and others. Chinese exports of a large variety of other categories of goods have also increased during the war. Russian banks have begun purchasing ATMs from China, after American companies refused to deliver and service them. In June, China announced it was ready to supply Russian airlines with spare parts. Several Chinese and Hong Kong law firms, including Zhong Yin, LT Lawyers, and CFN Lawyers, have announced plans to fill the void in Russia left by Western counterparts.

Chinese investments in Russia. Interestingly, no Chinese investments in Russia through the Belt and Road Initiative (BRI) were made throughout 2022. This is noteworthy, given that Russia is the largest foreign borrower for Chinese state banks and accounted for more than 15 percent of BRI lending between 2013 and 2017. On the other hand, data from 2022 indicate that Chinese banks have increased their lending to Russian customers through syndicated loans.

The “Yuanisation” of Russia

Russia has been rapidly increasing the use of yuan since the start of the war. China and Russia have long cooperated on “de-dollarization.” However, the war and sanctions have greatly accelerated this process, whereby Russia is increasingly reducing the use of dollars and euros and is increasingly using the yuan instead, a transition that has also been emphasised by Putin himself.

Russian reserves in yuan, and trade in yuan. Russia has rapidly intensified its use of yuan in many ways: two of the major ways are by expanding the proportion of yuan in its reserves, and increasingly switching to direct yuan-ruble trade, instead of using the dollar as an intermediary. In December 2022, the Russian Finance Department doubled the maximum allowable proportion of yuan in the Russian National Wealth Fund, from 30 to 60 percent. Yuan-ruble trading increased eightyfold between February and October 2022 (a total of 185 billion yuan, in October). The yuan’s share of the Russian currency market increased from 1 percent, in January, to over 48 percent in November, overtaking the dollar as the most traded foreign currency. Between January and September, the yuan’s share of all trade on the Russian stock market increased from 3 to 33 percent and, in February 2023, surpassed the dollar in trading volume. Chinese banks are, furthermore, accumulating more Russian assets.

Gas payments, digital currencies, and SWIFT alternatives. According to some sources, China has been paying with yuan for much its imports of Russian commodities over the past year, including oil, coal, and metals. In March 2023, Putin claimed that two-thirds of Russian-Chinese trade now was settled in either rubles or yuan. In September 2022, Gazprom and CNPC agreed to settle gas payments in ruble and yuan. Russia is also currently trying, together with China, to develop possibilities to use digital versions of their currencies (central bank digital currency, CBDC) for international payments, and also to thereby circumvent sanctions. The use of China’s SWIFT alternative, “CIPS” may also increase as Chinese banks trade more across the border with Russia, even if it may take a long time before this makes a significant difference for Russia.

Private use of yuan is also increasing. More and more Russian banks and companies, such as Sberbank; Rosneft; Rusal, the world's second-largest aluminium producer; the state-owned giant, Rosneft; and Polyus, the world’s fourth-largest gold producer, have also started to issue yuan bonds in Russia. Russian individuals are increasingly beginning to save in yuan, as more Russian banks, for example, VTB Bank and Tinkoff Bank offer this possibility. In September 2022, it was reported that VTB Bank was the first Russian bank to provide money transfers to China in yuan.

Problems and risks for Russia with the yuan. Despite all of this, there are currently many problems and risks for Russia with the use of the yuan. This includes yuan volatility, inconvertibility to other currencies, insufficiency in Russia, and imbalanced currency trade. The “yuanisation” of the Russian economy thereby also creates many vulnerabilities for Russia and strengthens China’s hand.

China’s strict control over the yuan exchange rates poses risks to Russia’s trade balance and gives China significant power over their trade. China exploited this to its advantage at the beginning of the invasion by allowing the value of the ruble against the yuan to fall more quickly, thereby protecting Beijing from sanctions against Moscow. Russia is also dependent on being able to sell off its yuan reserves, which it has also begun to do in 2023, to handle the budget deficit caused by low energy prices (although, reports in May suggested Russia might soon resume buying yuan instead of selling).

However, selling off the extensive and increasingly important reserves of yuan bonds may prove difficult if China were to limit the outflows of yuan, which gives China even more influence. Finally, the countries’ central banks have extensive “currency swap agreements” for the exchange of each other’s currencies. A new swap instrument was agreed upon in January 2023, for the purpose of increasing yuan availability in Russia and decreasing its volatility, which is used by Russian banks to increase yuan liquidity. However, the instrument also exposes China to the risk of secondary sanctions, a risk that could lead China to abandon these agreements, which in turn would have devastating consequences for Russia. All of this means that China gains political control over Russian reserves, trade, and payments.

De-dollarisation therefore means yuanisation. Both of the trends identified above – the increasing Russian use of the yuan in various ways, and the multitude of associated currency risks and problems – were acknowledged in an April 2023 report by the Russian Central Bank. Among other things, the report mentions the inconvertibility, insufficiency, restrictions, and need to sell off yuan in order to keep up the vital reserves of dollars, euros and other currencies.

In sum, for economic reasons, Russia is forced to turn to the yuan, which can strengthen the two countries’ relationship and trade, as well as mitigate the effects of the Western world’s sanctions. But the more Russia does this, the more economic and political power it hands over to China, and the more dependent it becomes on Chinese goodwill.

Cooperation on Trade Routes, Regionally and Across Borders

The cooperation on trade routes and infrastructure continues and is growing. Several new trade routes, such as new railway and multimodal transport routes that include several different means of transport, have been opened since the war began. In June 2022, the first ever car bridge between the countries was opened over the Amur River and, in November 2022, the first railway bridge. In March 2023 the first direct freight train between Beijing and Moscow departed, and plans for a second railway bridge across Amur was approved. In June 2023, an agreement was signed between FESCO and Russian Railways to accelerate rail transit of primarily cars between Russia and China, reflecting increasing Chinese vehicle exports to Russia (see above). Other planned or discussed projects include multimodal container routes; the development of a 2,000 km so-called “super highway,” Meridian, which would connect millions of Russians and Chinese; and the development of a common Russian-Chinese-Mongolian economic corridor.

The volume of cross-border trade is increasing sharply. According to Russian Railways, Russia’s railway freight traffic with China increased by 28 percent in 2022, compared to 2021, to a total of 123 million tons, and the state-owned company has been requesting the opening of two new railway lines across the border in the fall. In January 2023, freight traffic across the border reached record levels, according to Russian representatives. The Russian transport company, RUSCON, reported a fivefold increase in its container freight across the Russian-Chinese border in 2022, compared to 2021.

Regional economic cooperation. Chinese trade with and investment in Russia’s Far East is significant and increasing, aiming to facilitate Chinese import of Russian raw materials. Trade between China and Russia’s Far East increased by 28 percent in 2022 (totalling about USD14 billion) compared to 2021. The trade volume between the two neighbouring eastern regions, Primorsky Krai (Russia) and Heilongjiang (China), increased by more than 70 percent in the first half of 2022, according to Chinese customs.

Increasing trade between regions and across borders is also important for circumventing sanctions. According to Russian officials, trade between Russian and Chinese regions, as well as cross-border trade, is a significant source of growth and a priority in the development of the countries’ relations. They emphasised that this cooperation “has enormous anti-sanction potential, as it is not conducted at a macro level subject to external control, and because it offers more cooperation opportunities to small and medium-sized enterprises.” Key areas of cooperation mentioned include industry, agriculture, science, and people-to-people contacts.

Western weapons production still relies on Chinese exports via Russian railways. China supplies 90 percent of Europe’s use rare earth metals, which are crucial for the production of advanced weapon systems in the European defense industry. The significant portion of that export that goes through Russian railways more than doubled in 2022.

Conclusions

Relations between the countries have continued to develop in a positive direction in many areas during the war. In their political rhetoric, the two presidents and other high-ranking representatives have regularly emphasised that the relationship is strong, growing, resilient, and comprehensive, despite hostile global forces. The personal relationship between Putin and Xi is particularly highlighted. Even in the military field, relations continue to be strengthened, which is seen, among other things, in joint military exercises and ongoing cooperation in technological development.

In the economic sphere, relations have grown broadly. Trade recovered to record levels, from July 2022, onwards; Russian export of energy to China has increased significantly; and Chinese economic presence in, and export to, Russia has been strengthened considerably in many areas. Russian use of the yuan is growing, as is cooperation around trade routes, infrastructure and trade between regions and across the border.

In addition, China has provided important material support to Russian war efforts. Chinese exports of, among other things, integrated circuits, vehicles and other goods with dual-use applications, as well as metals and chemicals crucial for the Russian defense industry, have continued and, in some cases, significantly increased, during the war. However, China has provided no lethal weapons.

At the same time, the war has illuminated, and reinforced, the limitations of the relationship. The war is perhaps the most serious test of the relationship in several decades and demonstrates the many long-term, difficult challenges that it faces. Economic ties are limited by Russia’s fear of being exploited and, in more practical terms, by still insufficient infrastructure. China’s consideration of secondary sanctions, its reputation, and its economic relations with the Western world also present obstacles.

One of the most important effects of the war is to strengthen the long-standing trend towards a shift in the power balance, in China’s favour. Russia’s ongoing “yuanisation” is a clear example of this trend, as is the fact that Russia’s economy is now completely dependent on Chinese imports of Russian energy, and on Chinese exports of a multitude of goods, from cars to laptops and freezers.

However, it is also unclear when, how, and why China will utilise its increasing power over Russia. The dependency does not mean that Russia will become a Chinese vassal state, and it does not automatically translate into Chinese influence over Russia. China is likely to proceed cautiously, well aware of Russian sensitivities – such as its great power status, its independence, and its interests – and its dependence on Russia as a strategic partner and for its resources.

Russia will, however, likely have to come to terms with growing Chinese demands, whether they concern discounts on gas and oil; expanding Chinese presence in Russia, Central Asia, and the Arctic; access to Russian military technology; reduced Russian defense industrial cooperation with India; or support for China’s geopolitical ambitions in its vicinity. In the event of deteriorated relations, or increased Chinese fear of reactions from the Western world, China’s power may also be used against Russia. Regardless, China’s room for action will increase, and Russia’s will decrease.

References

[1] All trade data is from the General Administration of Customs of the People’s Republic of China. Russia stopped publishing its customs data in April 2022. Chinese customs data should of course be treated with caution.

[2] All data on Chinese energy payments to Russia is from 14 June, 2023.

[3] However, unlike its owner Geely, Volvo Cars stopped doing business in Russia after the invasion.

{kind=link}